The FinTech Impact Report: Working through the world’s to-do list

In today’s dynamic financial services landscape, the FinTech sector stands as a beacon of innovation and positive transformation.

FinTech

FinTech Innovation Lab

Report

People

Peace

Place

Planet

Productivity

Accenture

Data City

VestedImpact

Innovate Finance

Marketing

Interactive Content

Content

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact The FinTech Impact Report: Working through the world’s to-do list

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact "97% of the UK FinTech sector is a significant force for good across productivity, financial inclusion, peace and justice, but only 9% are having a positive impact on our planet." 2

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact Foreword A bold and honest outlook on the impact of FinTech In today’s dynamic financial services landscape, the blueprint on how that impact can be amplified across FinTech sector stands as a beacon of innovation and key challenge areas. positive transformation. Already significantly contributing to economic growth and employment By quantifying the FinTech sector’s impact, our hope is across the UK, the sector has also demonstrated over that we will enable key decision- and policy-makers the past decade its commitment to creating solutions across government, industry, regulators, and the private for other critical societal challenges – from the financial and public sectors to ensure the right solutions are crash of 2008, to the COVID-19 pandemic in 2021, to the being developed to support the growth of this thriving challenges afforded by the current cost of living and ecosystem. climate crises. As we face the global challenge of meeting the United As the UK FinTech industry continues to move from Nations’ 17 Sustainable Development Goals (SDGs), it is strength to strength, we wanted to find a way to critical – now more than ever – that we better measure the incredible impact the sector has already understand and harness the power of FinTech to drive made, and truly understand the potential that lies before forward progress and solutions across these priority it to bring even greater positive benefit to our world - to areas. This report assesses such impact as identify where and how FinTech can continue to comprehensively and effectively as possible, measuring contribute towards mitigating national and global over 500 FinTechs and traditional financial institutions in challenges that affect us all. how they contribute to the SDGs. This report aims to do just that – assessing and I hope the findings in this report inspire further action to analysing how FinTechs are delivering for the UK across accelerate the continued positive growth of our UK the areas of People, Planet, Place, Productivity, and FinTech sector - a sector which I believe is truly Peace, and where the gaps remain. It delves into the transforming financial services, and the world, for the impact the sector has made to date, and offers a better. Janine Hirt, CEO of Innovate Finance 3

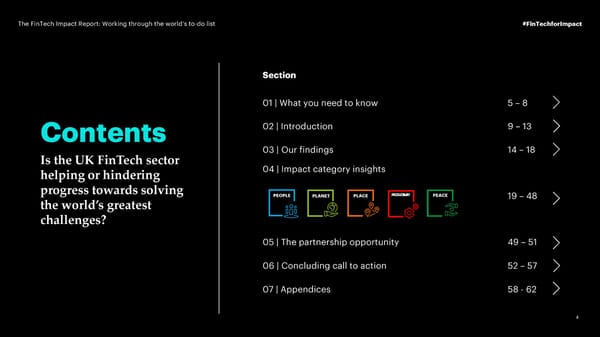

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact Section 01 | What you need to know 5 – 8 Contents 02 | Introduction 9 – 13 Is the UK FinTech sector 03 | Our findings 14 – 18 helping or hindering 04 | Impact category insights progress towards solving PEOPLE PLANET PLACE PRODUCTIVITY PEACE 19 – 48 the world’s greatest challenges? 05 | The partnership opportunity 49 – 51 06 | Concluding call to action 52 – 57 07 | Appendices 58 - 62 4

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact 01 | Whatyouneed toknow

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact FinTech is a force for good – giving people transparency, control and “connectivity to achieve better outcomes. Start-ups create solutions to the problems we face. Yet we tend to measure FinTech success in terms of funding rounds. “ This report answers a more fundamental question: what difference does it make? Adam Jackson Innovate Finance, Director of Policy

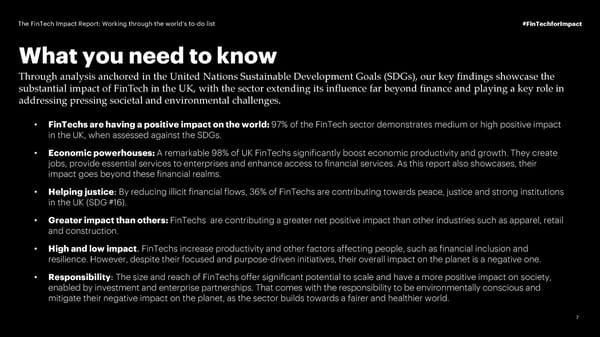

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact What you need to know Through analysis anchored in the United Nations Sustainable Development Goals (SDGs), our key findings showcase the substantial impact of FinTech in the UK, with the sector extending its influence far beyond finance and playing a key role in addressing pressing societal and environmental challenges. • FinTechs are having a positive impact on the world: 97% of the FinTech sector demonstrates medium or high positive impact in the UK, when assessed against the SDGs. • Economic powerhouses: A remarkable 98% of UK FinTechs significantly boost economic productivity and growth. They create jobs, provide essential services to enterprises and enhance access to financial services. As this report also showcases, their impact goes beyond these financial realms. • Helping justice: By reducing illicit financial flows, 36% of FinTechs are contributing towards peace, justice and strong institutions in the UK (SDG #16). • Greater impact than others: FinTechs are contributing a greater net positive impact than other industries such as apparel, retail and construction. • High and low impact. FinTechs increase productivity and other factors affecting people, such as financial inclusion and resilience. However, despite their focused and purpose-driven initiatives, their overall impact on the planet is a negative one. • Responsibility: The size and reach of FinTechs offer significant potential to scale and have a more positive impact on society, enabled by investment and enterprise partnerships. That comes with the responsibility to be environmentally conscious and mitigate their negative impact on the planet, as the sector builds towards a fairer and healthier world. 7

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact The true impact of FinTech on the world has – until now – gone “unmeasured and unreported. We wanted to change that. We want to not only hold ourselves accountable as a sector, but also “ enable FinTech to deliver on its promise at scale, through the power of partnerships. Graham Cressey Director, Accenture FinTech Innovation Lab

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact 02 |Introduction

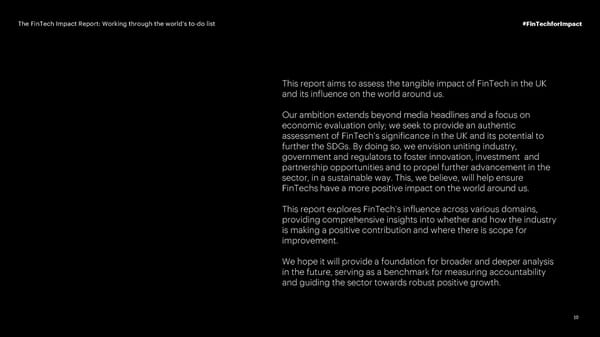

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact This report aims to assess the tangible impact of FinTech in the UK and its influence on the world around us. Our ambition extends beyond media headlines and a focus on economic evaluation only; we seek to provide an authentic assessment of FinTech’s significance in the UK and its potential to further the SDGs. By doing so, we envision uniting industry, government and regulators to foster innovation, investment and partnership opportunities and to propel further advancement in the sector, in a sustainable way. This, we believe, will help ensure FinTechs have a more positive impact on the world around us. This report explores FinTech’s influence across various domains, providing comprehensive insights into whether and how the industry is making a positive contribution and where there is scope for improvement. We hope it will provide a foundation for broader and deeper analysis in the future, serving as a benchmark for measuring accountability and guiding the sector towards robust positive growth. 10

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact ‘Impact’ is a regulatory and business imperative If they fail to understand their impact, organisations of all sizes run an increasing risk of losing their relevance in the market Regulations are evolving and today require more than inward-looking environmental, social and corporate governance (ESG) metrics. Companies today must assess and disclose their outward material impact. Directives such as the EU Corporate Sustainability Reporting Directive (CSRD) mandate that large firms and listed small and medium-sized enterprises (SMEs) evaluate and disclose the impact of their operations. This transition in regulations is unlikely to stop at the EU or at listed companies; a voluntary code is already being developed for non-listed SMEs operating in the EU1 and the FCA is consulting on 2 3 UK Sustainability Disclosure Requirements (SDR) as part of its ESG Strategy . Impact matters It’s a regulatory Moving beyond 94%to consumers requirement the ESG ‘tick box’ of consumers are more likely to be loyal to From 2024, companies operating and/or Incoming regulatory policies across the EU a company that is transparent about its located in the EU are required to report and UK require “science-based evidence” of 4 their ESG risks and impact risks. This impact; these include the EU CSRD and the environmental and social impact. includes listed SMEs. 5 Advertising Standards Agency Guidelines. 84%Access to 92%Regulation trickles 9%Few companies finance down to SMEs are ready of companies report incorporating ESG of buying organisations require their of companies assess sustainability “double into business practices has improved small business suppliers to disclose ESG materiality” (i.e. inward company impacts, 6 data, and 97% plan to increase their plus outward impact on the world); a their ability to raise investment funds requirements in 2024. 7 requirement of the incoming EU CSRD. 8 11

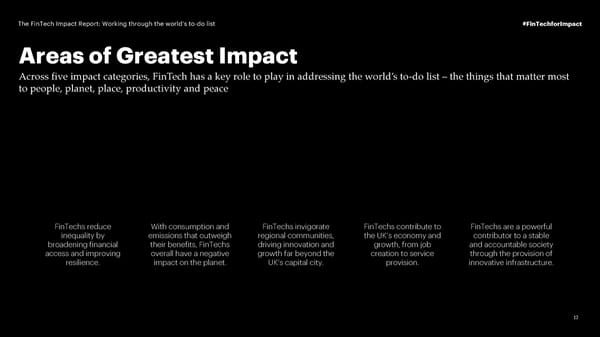

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact Areas of Greatest Impact Across five impact categories, FinTech has a key role to play in addressing the world’s to-do list – the things that matter most to people, planet, place, productivity and peace FinTechs reduce With consumption and FinTechs invigorate FinTechs contribute to FinTechs are a powerful inequality by emissions that outweigh regional communities, the UK’s economy and contributor to a stable broadening financial their benefits, FinTechs driving innovation and growth, from job and accountable society access and improving overall have a negative growth far beyond the creation to service through the provision of resilience. impact on the planet. UK’s capital city. provision. innovative infrastructure. 12

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact Defining impact against global goals Using the SDGs, we have devised a framework to assess the multi-faceted impact of FinTech in the UK across five impact categories: people, planet, place, productivity and peace 9 SDG Mapping The United Nations’ SDGs , established in 2015, are a comprehensive call to action aiming to eradicate poverty, safeguard our planet, and ensure PEOPLE prosperity and peace for all by 2030. As an unparalleled foundation for the assessment of impact, we organised the SDGs across five impact categories: people, planet, place, productivity and PLANET peace. Each category is directly and uniquely linked to the 17 SDGs, enabling us to holistically assess FinTech's influence on these underlying key areas. s eri A 500-strong representative sample of the UK’s biggest revenue generating go and most recently formed FinTechs was identified by The Data City. Then, ate PLACE delving beyond superficial assessments and internal operations, Vested Ct Impact assessed and mapped their business activities to the relevant UN SDG c pa targets, and we evaluated their broader societal and environmental Im contributions, and the communities they impact. PRODUCTIVITY Utilising Vested Impact’s proprietary algorithm, we analysed the depth of a company's impact based on the importance, value and effect of change the PEACE business activities contribute. This algorithm leverages over 300 million data points, including academic studies and scientific research, ensuring an evidence-based evaluation.10 If you wish to learn more about our approach, please see the Appendix. 13

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact 03 |Our Findings

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact The overall impact of FinTech FinTech is having a major impact on the SDGs, with 97% of the sector contributing a medium to very high positive impact. When assessed against the SDGs, a Net Impact Rating (NIR) can be FinTech Overall Share of FinTech sample calculated to demonstrate the intensity and quality of all the underlying Net Impact Rating; business activities for each company, against each of the issues they impact 1% Very High Impact Ove (whether positively, negatively or indirectly). (75-100) r a ll The UK’s FinTech sector has an overall NIR of 49, scoring higher than many 49 N 11 36% High Impact e other industries including capital markets, construction and retail. (50-74) t I Whilst FinTech scores lower than mpa sectors such as telecommunications ct and education which contribute so Capital Markets R a much to society, an impressive 97% -100 0 +100 ting of the UK’s FinTechs are having a (High Negative Impact) (Neutral Impact) (High Positive Impact) medium to very high positive impact 60% Medium Impact of (25-49) 12 F on the SDGs. in T e FinTech ch The overall NIR is a weighted aggregation of the 5 Gambling Apparel compa individual categories with a weighting added given Retail Telecom Low Impact some FinTechs impact multiple interconnected Services 2% (16-24) issues within categories. Construction ni Very Low Impact e Industry averages are based on the average of Education Services 1% s verified assets within each industry from Vested (0-15) : Impact’s database of +25,000 companies. 15

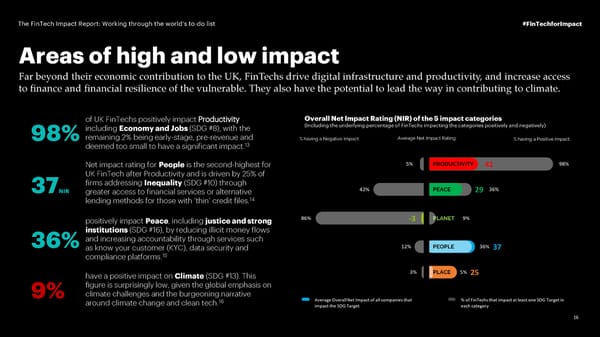

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact Areas of high and low impact Far beyond their economic contribution to the UK, FinTechs drive digital infrastructure and productivity, and increase access to finance and financial resilience of the vulnerable. They also have the potential to lead the way in contributing to climate. of UK FinTechs positively impact Productivity Overall Net Impact Rating (NIR) of the 5 impact categories including Economy and Jobs (SDG #8), with the (Including the underlying percentage of FinTechs impacting the categories positively and negatively) 98%remaining 2% being early-stage, pre-revenue and deemed too small to have a significant impact.13 Net impact rating for People is the second-highest for UK FinTech after Productivity and is driven by 25% of 37NIR firms addressing Inequality (SDG #10) through greater access to financial services or alternative 14 lending methods for those with ‘thin’ credit files. positively impact Peace, including justice and strong institutions (SDG #16), by reducing illicit money flows 36%and increasing accountability through services such as know your customer (KYC), data security and compliance platforms.15 have a positive impact on Climate (SDG #13). This figure is surprisingly low, given the global emphasis on 9% climate challenges and the burgeoning narrative around climate change and clean tech.16 16

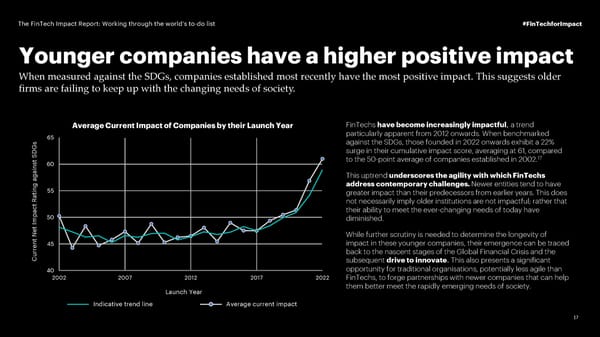

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact Younger companies have a higher positive impact When measured against the SDGs, companies established most recently have the most positive impact. This suggests older firms are failing to keep up with the changing needs of society. Average Current Impact of Companies by their Launch Year FinTechs have become increasingly impactful, a trend 65 particularly apparent from 2012 onwards. When benchmarked sG against the SDGs, those founded in 2022 onwards exhibit a 22% SD surge in their cumulative impact score, averaging at 61, compared t to the 50-point average of companies established in 2002.17 ins60 aga This uptrend underscores the agility with which FinTechs address contemporary challenges. Newer entities tend to have ing 55 greater impact than their predecessors from earlier years. This does Rat not necessarily imply older institutions are not impactful; rather that pact their ability to meet the ever-changing needs of today have Im50 diminished. Net While further scrutiny is needed to determine the longevity of ent 45 impact in these younger companies, their emergence can be traced rru back to the nascent stages of the Global Financial Crisis and the C subsequent drive to innovate. This also presents a significant 40 opportunity for traditional organisations, potentially less agile than 2002 2007 2012 2017 2022 FinTechs, to forge partnerships with newer companies that can help Launch Year them better meet the rapidly emerging needs of society. Indicative trend line Average current impact 17

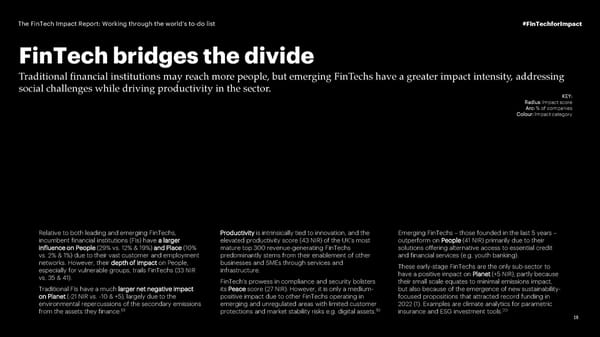

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact FinTech bridges the divide Traditional financial institutions may reach more people, but emerging FinTechs have a greater impact intensity, addressing social challenges while driving productivity in the sector. KEY: Radius: Impact score Arc: % of companies Colour: Impact category Relative to both leading and emerging FinTechs, Productivity is intrinsically tied to innovation, and the Emerging FinTechs – those founded in the last 5 years – incumbent financial institutions (FIs) have a larger elevated productivity score (43 NIR) of the UK’s most outperform on People (41 NIR) primarily due to their influence on People (29% vs. 12% & 19%) and Place (10% mature top 300 revenue-generating FinTechs solutions offering alternative access to essential credit vs. 2% & 1%) due to their vast customer and employment predominantly stems from their enablement of other and financial services (e.g. youth banking). networks. However, their depth of impact on People, businesses and SMEs through services and These early-stage FinTechs are the only sub-sector to especially for vulnerable groups, trails FinTechs (33 NIR infrastructure. have a positive impact on Planet (+5 NIR), partly because vs. 35 & 41). FinTech’s prowess in compliance and security bolsters their small scale equates to minimal emissions impact, Traditional FIs have a much larger net negative impact its Peace score (27 NIR). However, it is only a medium- but also because of the emergence of new sustainability- on Planet (-21 NIR vs. -10 & +5), largely due to the positive impact due to other FinTechs operating in focused propositions that attracted record funding in environmental repercussions of the secondary emissions emerging and unregulated areas with limited customer 2022 (1). Examples are climate analytics for parametric 19 19 20 from the assets they finance. protections and market stability risks e.g. digital assets. insurance and ESG investment tools. 18

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact 04 |Impact Category Insights

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPeople FinTechs reduce inequality by broadening financial access and improving resilience. 21 Access to financial services is a vital factor for coping with and escaping poverty . It is why the United Nations includes it in 7 out of 17 of its Sustainable Development Goals, as an essential factor for improving the condition of the most marginalised citizens. FinTechs are helping to reduce this inequality through their services to extend credit lines and open-up access to financial services. However, with underrepresentation of females in FinTech executive roles (20%) and the broader workforce (28% vs. 44% in Financial Services) as well as a persistent gender pay gap, more needs to be done for equality within FinTech – a point that Innovate Finance’s recent Women in FinTech and Annual FinTech Investment Reports draw out clearly. 22

FinTech for Impact: Working through the world’s to-do list #FinTechforPeople The FinTech sector is now an established component of the UK economy and continues to show great promise. “ However, the sector remains a male dominated industry with data clearly showing that it lags behind national averages on numbers of women as directors, the number of women led FinTechs and particularly discouragingly, that women led FinTech businesses are significantly less likely to secure “ private investment than in other sectors. Whilst the FinTech sector is clearly an economic success story, it is not an inclusive growth story. Alex Craven Co-Founder, The Data City

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPeople PEOPLE This impact category spans poverty to education to inequality. FinTech has an overall positive impact, with 36% of firms directly contributing 23 versus the 12% of FinTechs registering a negative impact. Key SDG targets impacting People: (Including the percentage of FinTechs and their average Net Impact Ratings) FinTechs are… 01 | Boosting financial inclusion with access to banking services 02| Reducing inequality through provision of alternative finance But there is still work to do… 03| Ill-secured products and services cause financial insecurity 04 | Remittances are still too costly 05 | Current identity verification practices exacerbate inequality 06 | The gender gap in FinTech needs to be addressed 07 | The underserved financial market is growing 22

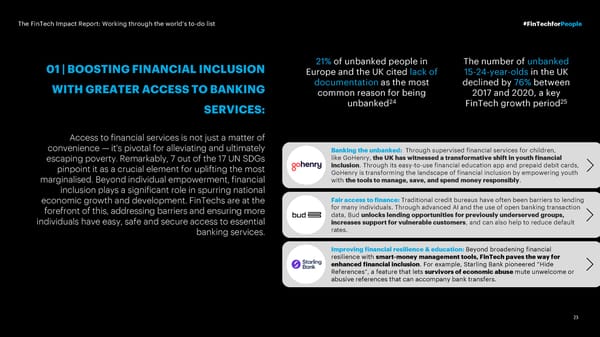

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPeople 01 | BOOSTING FINANCIAL INCLUSION 21% of unbanked people in The number of unbanked Europe and the UK cited lack of 15-24-year-olds in the UK WITH GREATER ACCESS TO BANKING documentationas the most declined by 76% between common reason for being 2017 and 2020, a key SERVICES: unbanked24 FinTech growth period25 Access to financial services is not just a matter of convenience — it's pivotal for alleviating and ultimately Banking the unbanked: Through supervised financial services for children, escaping poverty. Remarkably, 7 out of the 17 UN SDGs like GoHenry, the UK has witnessed a transformative shift in youth financial pinpoint it as a crucial element for uplifting the most inclusion. Through its easy-to-use financial education app and prepaid debit cards, GoHenry is transforming the landscape of financial inclusion by empowering youth marginalised. Beyond individual empowerment, financial with the tools to manage, save, and spend money responsibly. inclusion plays a significant role in spurring national economic growth and development. FinTechs are at the Fair access to finance: Traditional credit bureaus have often been barriers to lending forefront of this, addressing barriers and ensuring more for many individuals. Through advanced AI and the use of open banking transaction individuals have easy, safe and secure access to essential data, Bud unlocks lending opportunities for previously underserved groups, increases support for vulnerable customers, and can also help to reduce default banking services. rates. Improving financial resilience & education: Beyond broadening financial resilience with smart-money management tools, FinTech paves the way for enhanced financial inclusion. For example, Starling Bank pioneered “Hide References”, a feature that lets survivors of economic abuse mute unwelcome or abusive references that can accompany bank transfers. 23

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPeople 02| REDUCING INEQUALITY THROUGH 1/3 of the 1.3 million 1 in 4 UK adults have low unbanked in the UK used to financial resilience in have a bank account but terms of savings and debt PROVISION OF ALTERNATIVE FINANCE: 26 don’t want one again levels, putting them at risk if they suffer a financial shock27 Alternative finance typically operates outside the confines of traditional financial solutions, offering innovative channels, processes, and instruments. Distinctly Championing Diversity in Funding:Founded off the back of the ‘Over Being characterised by their simplicity, speed, and accessibility, Underfunded’ campaign, which successfully changed legislation to make investment these financing methods cater specifically to underserved more accessible for early-stage entrepreneurs, Obu's platform takes a decisive stand in closing the gender investment gap in the UK for both entrepreneurs and angel individuals, startups, and businesses, enabling them to investors. Obu exists to increase the number of women angel investors in the UK from efficiently raise, invest, and manage their funds. 14% to 30%, thereby increasing the level of investment placed in businesses founded by women. Redefining Cross-Border Transactions: By fundamentally reimagining international remittances and multi-currency services, Wise has set new industry standards for affordability and efficiency. Reducing the speed and cost barriers commonly associated with cross-border transfers, Wise has scaled its impact to approximately 16 million global users, directly contributing to a reduction in financial inequality. Fair access to public markets: Primary Bid's platform democratises investment, allowing retail investors to participate in new share issues — opportunities historically reserved for institutional investors or high-net-worth individuals. By leveraging technology, PrimaryBid is dedicated to the ethos of inclusivity, transparency, and fairness in public markets. 24

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPeople But there is still work to do… 03 | ILL-SECURED PRODUCTS / SERVICES CAUSE FINANCIAL 19% of the FinTechs we assessed INSECURITY have some form of negative impact Digital innovations have revolutionised access to finance, but in some cases they also expose on people, where on average it is a customers to new unregulated risks and the potential for financial loss from early iterations of new 28 asset classes and alternative market platforms. Early regulator engagement, alongside greater very low negative impact. awareness and responsibility in founding teams, is required in light of the potential impact these propositions can have on customers and markets. 04 | REMITTANCES ARE STILL TOO COSTLY UK remitters paid £304 million more The UK’s average costs have gone down by an average of 0.06% per quarter since the ‘Reduced in 2022 than they would have if Inequality’ SDG Number 10 was introduced in Q3 2015.30 This rate of progress is too slow for the UK to companies had priced transactions come close to reaching the

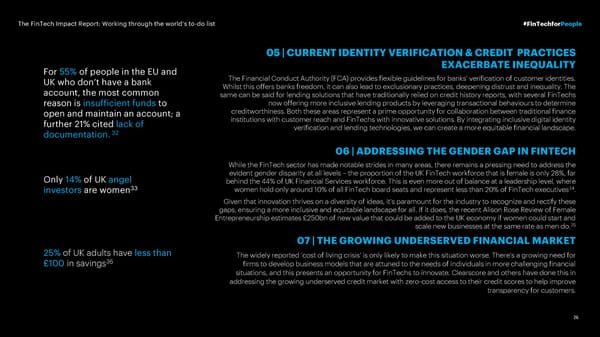

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPeople 05 | CURRENT IDENTITY VERIFICATION & CREDIT PRACTICES For 55% of people in the EU and EXACERBATE INEQUALITY The Financial Conduct Authority (FCA) provides flexible guidelines for banks’ verification of customer identities. UK who don’t have a bank Whilst this offers banks freedom, it can also lead to exclusionary practices, deepening distrust and inequality. The account, the most common same can be said for lending solutions that have traditionally relied on credit history reports, with several FinTechs reason is insufficient funds to now offering more inclusive lending products by leveraging transactional behaviours to determine open and maintain an account; a creditworthiness. Both these areas represent a prime opportunity for collaboration between traditional finance further 21% cited lack of institutions with customer reach and FinTechs with innovative solutions. By integrating inclusive digital identity documentation.32 verification and lending technologies, we can create a more equitable financial landscape. 06 | ADDRESSING THE GENDER GAP IN FINTECH While the FinTech sector has made notable strides in many areas, there remains a pressing need to address the Only 14% of UK angel evident gender disparity at all levels – the proportion of the UK FinTech workforce that is female is only 28%, far behind the 44% of UK Financial Services workforce. This is even more out of balance at a leadership level, where 33 women hold only around 10% of all FinTech board seats and represent less than 20% of FinTech executives34. investors are women Given that innovation thrives on a diversity of ideas, it's paramount for the industry to recognize and rectify these gaps, ensuring a more inclusive and equitable landscape for all. If it does, the recent Alison Rose Review of Female Entrepreneurship estimates £250bn of new value that could be added to the UK economy if women could start and scale new businesses at the same rate as men do.35 07 | THE GROWING UNDERSERVED FINANCIAL MARKET 25% of UK adults have less than The widely reported ‘cost of living crisis’ is only likely to make this situation worse. There's a growing need for £100 in savings36 firms to develop business models that are attuned to the needs of individuals in more challenging financial situations, and this presents an opportunity for FinTechs to innovate. Clearscore and others have done this in addressing the growing underserved credit market with zero-cost access to their credit scores to help improve transparency for customers. 26

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPlanet Only 9% of FinTechs are having a positive impact on the planet, with consumption and emissions outweighing their benefits Planet is the only impact category with an overall negative Net Impact Rating (NIR) in our assessment. This is driven largely by the emissions impact of FinTech. Indirect greenhouse gas (GHG) emissions associated with 37 financial institutions’ investing, lending and underwriting are on average over 700 times higher than the direct emissions that come from daily operations. To mitigate this negative impact, FinTechs will need to provide sustainable financing, consume clean energy and minimise e-waste. They will also need to extend the practices they’ve pioneered, such as analytics for Impact Investing and digital services that reduce paper consumption. They should also minimise the need for travel between physical places.

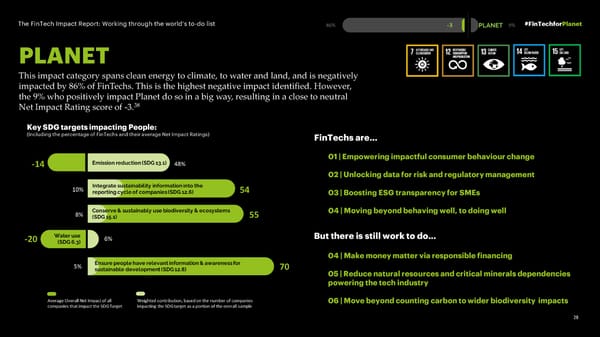

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPlanet PLANET This impact category spans clean energy to climate, to water and land, and is negatively impacted by 86% of FinTechs. This is the highest negative impact identified. However, the 9% who positively impact Planet do so in a big way, resulting in a close to neutral 38 Net Impact Rating score of -3. Key SDG targets impacting People: (Including the percentage of FinTechs and their average Net Impact Ratings) FinTechs are… 01 | Empowering impactful consumer behaviour change 02 | Unlocking data for risk and regulatory management 03 | Boosting ESG transparency for SMEs 04 | Moving beyond behaving well, to doing well But there is still work to do… 04 | Make money matter via responsible financing 05 | Reduce natural resources and critical minerals dependencies powering the tech industry 06 | Move beyond counting carbon to wider biodiversity impacts 28

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPlanet 01 | EMPOWERING IMPACTFUL 95% of millennials say 59% of Britons are making they care about conscious decisions to live a CONSUMER BEHAVIOUR CHANGE sustainable investing41 low-carbon lifestyle42 Purpose-driven ‘impact investing’ is gaining strong momentum, with 63% growth in the private impact 39 market between 2019 and 2021 . And the data shows 59% of Britons are making conscious decisions to live a Investing in a better future: The FinTech CIRCA5000 (previously tickr) launched low-carbon lifestyle, including 17% who make these impact Exchange Traded Funds (ETFs) covering the investible SDGs. Their 40 range of ETFs includes Green Energy & Technology and Clean Water & Waste. decisions even when it is inconvenient for them . Thousands of retail investors use the CIRCA5000 investing app, and CIRCA5000 is the first pure-play impact ETF issuer in Europe. Empowering consumers with the products and data to Connecting carbon data and behavioural science to compel climate action: Cogo's make more conscious financial and behavioural decisions carbon footprint calculator helps individuals and businesses measure, understand in line with their lifestyle and values is critical to educating and reduce their carbon impact. Cogo uses best-in-class models to provide accurate them, and ultimately driving sustainable progress in ways to measure carbon emissions specific to local markets and cutting-edge reducing emissions and environmental impacts. behavioural science techniques to nudge customers to make more sustainable choices. Cogo is a Certified B Corporation and is aiming to become the world's first gigacorn. 29

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPlanet 02 | UNLOCKING DATA FOR RISK AND Less than 20% of It is estimated that institutional companies quantify investors spend an average impact, despite 96% $1.3m a year on sustainability REGULATORY MANAGEMENT producing ESG reports44 and ESG data45 Improving the sustainability of asset management and lending is one of the highest impact areas for FinTech. The indirect greenhouse gas (GHG) emissions associated with Quantify climate risk: Climate X, a global climate risk data provider, helps financial institutions’ investing, lending and underwriting organisations assess exposure to extreme weather events (flood, drought, 43 activities are on average over 700 times higher than the subsidence, etc.) for various RCP/SSPs between now and the year 2100 - in direct emissions that come from their daily operations. seconds. Aligned with the latest regulations, Climate X data enables stress testing and back-book analysis, yielding better-informed commercial decisions. FinTechs lead the way in providing the data for financial and environmental risk management to support Using data to mobilise capital towards sustainability: U Impact’s white-label fund compliance of financial institutions, investors and exploration and behavioural analytics suite helps to empower the new generation companies with increasing regulations. They also provide of sustainability-conscious investors with better information on the funds to invest in. This helps move capital in ways that contribute to reaching the SDGs. the data to evidence and secure lending and debt finance against critical social and environmental targets. 30

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPlanet 03 | BOOSTING ESG TRANSPARENCY 45% of UK SMEs 84% of companies report recognise it is incorporating ESG into FOR SMES important to lower business practices has their emissions in the improved their ability to raise 49 50 near future. investment funds. 87% of UK SMEs are unaware of their business’ total 46 carbon emissions, despite good intentions. And yet, the UK’s six million SMEs can contribute to up to 50% of the Know your impact: Vested Impact offers automated, impact assessment for UK’s net zero decarbonisation goals by 2030, worth an companies and investors, leveraging over 300 million science-based and impact estimated £160 billion in revenue.47 data points to assess what a company impacts outwardly, across over 169 UN SDG targets, aligning with global standards and regulations, supplying data to the likes The increasing regulatory burdens on large businesses of the United Nations, and currently expanding their platform to over 1.2m SMEs. are also flowing down onto SMEs in their supply chains. The proportion of major buying organisations that The role of FinTech in Net-Zero: Innovate Finance’s report identified several areas require their SME suppliers to disclose ESG information is FinTech can build a net-zero world that closely align to our findings here including 48 enabling consumers to take action and enabling financial institutions’ 51 expected to reach 92% in 2024. Incoming regulations compliance with climate risk regulation. It also called for adoption of science- like the EU CSRD will require reporting beyond just based CO2 reduction across operations and supply chains and advocated for the emissions and will include outward risks. FinTech is power of FinTech tools and technologies to enable other businesses to develop NetZero operations and products. already innovating in the provision of simple data sources and streamlined reporting to help SMEs be compliant and position for a competitive advantage. 31

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPlanet 04 | MOVING BEYOND BEHAVING WELL From 2024, more than ~50,000 companies in Europe, and thousands in the UK, will be required to report their outward TO DOING WELL material impacts on society, and biodiversity and environment (under EU CSRD).53 Sustainable development areas beyond climate need to be considered for the good of society and the planet, such as biodiversity, water and the social impacts of inequality and poverty. The Task Force on Nature- Nurture the World: Uniting humanitarian, financial and technology sectors, F4ID related Financial Disclosures (TNFD) is currently drafting provides a digital supply and payments platform for aid organisations, enabling local vendors to give life-saving assistance to vulnerable households in the most hostile a framework that will help financial institutions identify environments. Through its LOTUS20 pilot programme in Kenya, Afghanistan and 52 Nigeria, 170+ tonnes of food reached 10,000 people, with every transaction nature-related risks. tracked in real-time. As this agenda evolves, new opportunities will continue Connect to Charities Percent gives non-profits access to fundraising options and to emerge for FinTechs to not just behave well, but also discounted tech products through partnerships. Its global disbursement system to be the financial services enablers that help others to enables businesses to integrate fundraising into its platform, with the ability to do well regarding the issues that matter most to disburse funds to over 5.7 million non-profits across 200+ countries. communities and the planet. 32

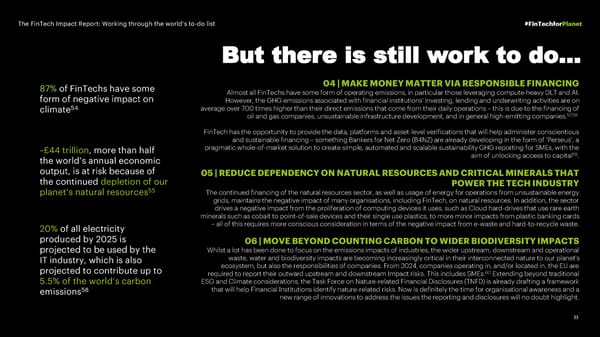

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPlanet But there is still work to do… 87% of FinTechs have some 04 | MAKE MONEY MATTER VIA RESPONSIBLE FINANCING form of negative impact on Almost all FinTechs have some form of operating emissions, in particular those leveraging compute-heavy DLT and AI. However, the GHG emissions associated with financial institutions' investing, lending and underwriting activities are on climate54 average over 700 times higher than their direct emissions that come from their daily operations – this is due to the financing of oil and gas companies, unsustainable infrastructure development, and in general high-emitting companies.57,58 FinTech has the opportunity to provide the data, platforms and asset-level verifications that will help administer conscientious and sustainable financing – something Bankers for Net Zero (B4NZ) are already developing in the form of ‘Perseus’, a ~£44 trillion, more than half pragmatic whole-of-market solution to create simple, automated and scalable sustainability GHG reporting for SMEs, with the 59 aim of unlocking access to capital . the world’s annual economic output, is at risk because of 05 | REDUCE DEPENDENCY ON NATURAL RESOURCES AND CRITICAL MINERALS THAT the continued depletion of our POWER THE TECH INDUSTRY planet’s natural resources55 The continued financing of the natural resources sector, as well as usage of energy for operations from unsustainable energy grids, maintains the negative impact of many organisations, including FinTech, on natural resources. In addition, the sector drives a negative impact from the proliferation of computing devices it uses, such as Cloud hard-drives that use rare earth minerals such as cobalt to point-of-sale devices and their single use plastics, to more minor impacts from plastic banking cards 20% of all electricity – all of this requires more conscious consideration in terms of the negative impact from e-waste and hard-to-recycle waste. produced by 2025 is 06 | MOVE BEYOND COUNTING CARBON TO WIDER BIODIVERSITYIMPACTS projected to be used by the Whilst a lot has been done to focus on the emissions impacts of industries, the wider upstream, downstream and operational IT industry, which is also waste, water and biodiversity impacts are becoming increasingly critical in their interconnected nature to our planet's projected to contribute up to ecosystem, but also the responsibilities of companies. From 2024, companies operating in, and/or located in, the EU are 60 required to report their outward upstream and downstream Impact risks. This includes SMEs. Extending beyond traditional ESG and Climate considerations, the Task Force on Nature-related Financial Disclosures (TNFD) is already drafting a framework 5.5% of the world’s carbon emissions56 that will help Financial Institutions identify nature-related risks. Now is definitely the time for organisational awareness and a new range of innovations to address the issues the reporting and disclosures will no doubt highlight. 33

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPlace FinTechs invigorate regional communities, increasingly driving innovation and growth beyond London. FinTechs are catalysing regional growth across the UK, infusing vitality into areas beyond the capital city through job creation and fostering of vibrant local cultures. From Starling Bank anchoring its operations in Cardiff and Southampton, to Atom Bank taking root in Durham, the impact is tangible and relatively widespread. Beyond their own footprint, FinTechs are reshaping our cities and communities with innovative mortgage platforms that simplify home buying and smart financing solutions for electric vehicle fleets. These offer fresh avenues of relief for those grappling with rising rents, mortgage and transportation costs amidst the cost of living crisis.

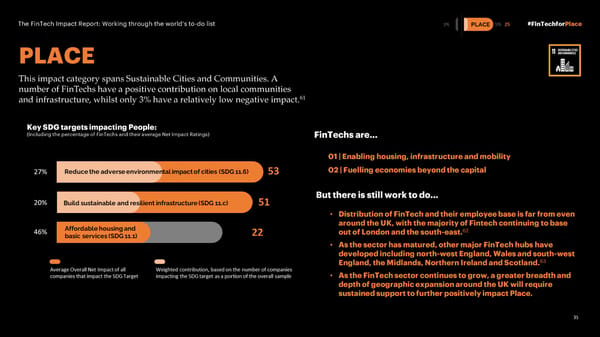

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPlace PLACE This impact category spans Sustainable Cities and Communities. A number of FinTechs have a positive contribution on local communities 61 and infrastructure, whilst only 3% have a relatively low negative impact. Key SDG targets impacting People: (Including the percentage of FinTechs and their average Net Impact Ratings) FinTechs are… 01 | Enabling housing, infrastructure and mobility 02 | Fuelling economies beyond the capital But there is still work to do… • Distribution of FinTech and their employee base is far from even around the UK, with the majority of Fintech continuing to base 62 out of London and the south-east. • As the sector has matured, other major FinTech hubs have developed including north-west England, Wales and south-west England, the Midlands, Northern Ireland and Scotland.63 • As the FinTech sector continues to grow, a greater breadth and depth of geographic expansion around the UK will require sustained support to further positively impact Place. 35

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPlace 01 | ENABLING HOUSING, 5% of the UK’s FinTechs have The number of households a direct positive impact on facing eviction in the private sustainable cities and rented sector is at its INFRASTRUCTURE & MOBILITY 64 65 communities in the UK. highest in 8 years. Traditional finance has a significant positive impact on housing and infrastructure through the provision of mortgages. In the assessment against the SDGs, the impact of FinTech on housing is a mixed story. The related Clean Mobility Transition: A digital financing platform, Zeti connects operators of business activities are more service- and platform-led than business-critical vehicle fleets transitioning to clean transport with institutional pure financing, and the positive benefits to homebuyers of funders. Zeti's technology enables flexible risk-adjusted finance and value-added data services to both lenders and borrowers. Zeti pioneered a low-cost pay-per-mile accessible, mobile-friendly digital mortgages are somewhat model to transition $40m of fleets to electric vehicles, saving ~7 million kg of CO2 in offset by their reduced affordability. This is because the the process. more accessible digital services facilitate greater market Simplified Home Buying: Koodoo has taken mortgages digital, streamlining the access, causing an upward pressure on purchase prices. search and application processes to make it quicker for customers to purchase or refinance a home. Koodoo enables mortgage providers to surface the right products to borrowers via comparison sites, and allows customers to apply directly FinTechs have been at the forefront of enabling greater to lenders, or speak to a broker if they need more support in the process. mobility in UK cities by partnering with transport providers for seamless payments and loyalty schemes. Over ten years on since the significant step forward in contactless payments that Transport for London (TFL) facilitated, app-based micro-transport providers of carpools, bikes and scooters has proliferated embedded payments in recent years. 36

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPlace 02 | FUELLING ECONOMIES BEYOND THE People are 7 times more likely Only 3% of the FinTechs we to be in financial difficulty in assessed have some form of CAPITAL the most deprived areas of negative impact on Place; on the UK compared to those in average it is a low negative 67 68 the least deprived areas. impact. London is renowned as a global hub for FinTechand still hosts about the majority of the UK FinTech sector. Firms are however increasingly located in other cities such as Manchester, Leeds, Edinburgh, Durham and Cardiff to secure more talent, access financial incentives and improve 66 Innovating across the UK: The Centre for Finance, Innovation and Technology their staff’s living standards. (CFIT) was set up following the Kalifa Review of Fintech (2021) to position the UK as a global leader in financial innovation. It has already launched activities across the UK, bringing multiple organisations together to tackle the pressing FinTechs have a strong presence in these regions, with challenge of Open Finance that will unlock new growth for financial services. initiatives – including associated industry bodies that are part of the FinTech National Network – promoting regional FinTech National Network: Regional FinTech hubs drive a range of activities across local development and boosting economic activity and local job companies, including industry roundtables, events and partnership support. This is helping improve communities, make workplaces more appealing, and support the founding of local creation. There are also regional accelerators that go businesses. It all contributes to thriving innovation and a boost to the local economies. beyond FinTech to help start-ups of all types to grow, such as Atom’s Incubator, NatWest’s Entrepreneur Accelerator and Barclays’ Eagle Labs. 37

The FinTech Impact Report: Working through the world’s to-do list #FinTechforProductivity 98% of UK FinTechs are contributing to the growth of the economy, from job creation to service provision UK FinTech represents a significant industry sector driving economic prosperity, fostering growth, 69 and ushering in innovation . By catalysing economic expansion, deploying vital infrastructure, expanding financial access for SMEs and nurturing entrepreneurship, FinTechs help shape a robust and vibrant economic landscape for the UK. 38

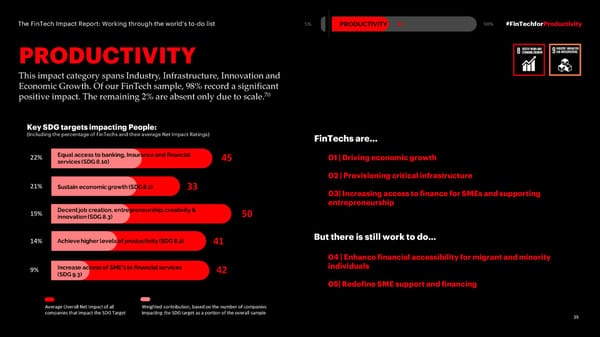

The FinTech Impact Report: Working through the world’s to-do list #FinTechforProductivity PRODUCTIVITY This impact category spans Industry, Infrastructure, Innovation and Economic Growth. Of our FinTech sample, 98% record a significant 70 positive impact. The remaining 2% are absent only due to scale. Key SDG targets impacting People: (Including the percentage of FinTechs and their average Net Impact Ratings) FinTechs are… 01 | Driving economic growth 02 | Provisioning critical infrastructure 03| Increasing access to finance for SMEs and supporting entrepreneurship But there is still work to do… 04 | Enhance financial accessibility for migrant and minority individuals 05| Redefine SME support and financing 39

The FinTech Impact Report: Working through the world’s to-do list #FinTechforProductivity 01 | DRIVING ECONOMIC GROWTH 98% of UK FinTechs The collective value contribute to economic of the UK’s top 10 73 74 By their nature as start-up companies working in the UK, productivity and growth FinTechs is $60bn 98% of the UK’s FinTechs positively impact Productivity including Economy and Jobs (SDG #8). The remaining 2% are early-stage, pre-revenue and deemed too small to be having a significant impact at this stage.71 As an increasingly mature sector of the economy, the UK is Easy money management: Revolut is a global financial super app, designed to simplify all things money. It helps its customers spend, save, invest, budget or now home to 21 of the UK’s 44 unicorn companies borrow, in a frictionless, easy to use way. The company has over 30 million including Monzo, Revolut and Wise. 72 customers worldwide across 38 countries, who together make half a billion transactions a month, and employs over 7,000 employees globally. Encouragingly, there has been strong Government and Smarter lending, bigger savings: Utilising advanced AI and machine learning, Zopa industry support for furthering the UK’s position as a Bank delivers fair and transparent products that offer great value to consumers leading FinTech hub. For example, the Kalifa Review of UK while delivering strong credit performance. As a fully licensed bank, it serves 1 FinTech (2021) led to the establishment of the Centre for million customers with a diverse product range, including personal loans, car finance, credit cards, & award-winning savings accounts. It also provides tools for Financial Innovation & Technology (CFIT, 2023). This improved financial management and health. presents an opportunity to drive real momentum into the sector despite recent challenges with investment funding in a rising-interest-rate environment. 40

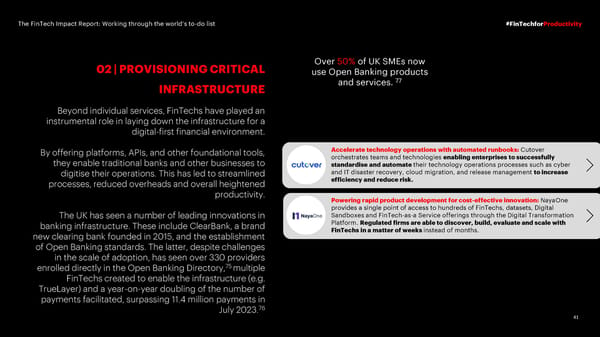

The FinTech Impact Report: Working through the world’s to-do list #FinTechforProductivity 02 | PROVISIONING CRITICAL Over 50% of UK SMEs now use Open Banking products 77 INFRASTRUCTURE and services. Beyond individual services, FinTechs have played an instrumental role in laying down the infrastructure for a digital-first financial environment. By offering platforms, APIs, and other foundational tools, Accelerate technology operations with automated runbooks: Cutover they enable traditional banks and other businesses to orchestrates teams and technologies enabling enterprises to successfully standardise and automate their technology operations processes such as cyber digitise their operations. This has led to streamlined and IT disaster recovery, cloud migration, and release management to increase processes, reduced overheads and overall heightened efficiency and reduce risk. productivity. Powering rapid product development for cost-effective innovation: NayaOne provides a single point of access to hundreds of FinTechs, datasets, Digital The UK has seen a number of leading innovations in Sandboxes and FinTech-as-a Service offerings through the Digital Transformation banking infrastructure. These include ClearBank, a brand Platform. Regulated firms are able to discover, build, evaluate and scale with new clearing bank founded in 2015, and the establishment FinTechs in a matter of weeks instead of months. of Open Banking standards. The latter, despite challenges in the scale of adoption, has seen over 330 providers 75 enrolled directly in the Open Banking Directory, multiple FinTechs created to enable the infrastructure (e.g. TrueLayer) and a year-on-year doubling of the number of payments facilitated, surpassing 11.4 million payments in 76 July 2023. 41

The FinTech Impact Report: Working through the world’s to-do list #FinTechforProductivity 03 | INCREASING ACCESS TO FINANCE 35% of FinTechs are Over 50% of all UK SME delivering products and finance is provided by FOR SMEs AND SUPPORTING services that are directed at FinTech challenger banks and significantly impact and alternative finance 78 79 ENTREPRENEURSHIP other SMEs. providers. One of the most transformative impacts of FinTech has been its provision of services to SMEs. Most notable is its Fast flexible debt finance for the ‘Missing Middle’: OakNorth financing takes a more efficient provision of finance, which traditional banks have forward-looking and data-driven approach to credit decisioning, providing historically struggled to achieve due to the often complex businesses with access to fast and flexible debt finance ranging from £250k to tens nature of the offering and the urgency of the need. of millions of pounds. Since its launch in 2015, OakNorth has lent c.£10bn directly helping with the creation of 37,000 new jobs and 27,000 new homes across the UK. A number of FinTechs have identified and quickly bridged A leading business financial platform in the UK: Tide helps SMEs save time (and money) in the running of their businesses by not only offering business accounts this gap; an example is Iwoca’s digital lending solutions. and related banking services, but also a comprehensive set of highly usable and Moreover, beyond simply providing essential credit, connected administrative solutions from invoicing to accounting. Tide has 550k FinTechs have innovated in the surrounding services that SME members in the UK (10% market share) and more than 150k SMEs in India. help SMEs become more efficient and grow their own businesses. Whether improving their cashflow with invoice Bespoke custom-built financing solutions for small businesses: Iwoca’s partner financing or integrating accountancy tools like Xero, integrations and lending APIs help small businesses gain access to finance when and where they need it. Iwoca has an award-winning credit risk engine that FinTech has furnished SMEs facilitates faster, more accurate credit decisions. This has expanded financing with a plethora of tailored services. possibilities for small businesses. 42

The FinTech Impact Report: Working through the world’s to-do list #FinTechforProductivity But there is still work to do… 04 | ENHANCING FINANCIAL ACCESSIBILITY FOR MIGRANT AND MINORITY INDIVIDUALS 1/3 of founders in the UK The UK's diverse entrepreneurial landscape is enriched by the contributions of non-British founders, who constitute aren’t British and have roughly a third of the total. These individuals bring innovative ideas, novel perspectives, and international networks, challenges setting up playing a pivotal role in fostering economic growth and global competitiveness. However, as reported by Sifted, when 80 they face barriers in accessing the UK's banking system, the entire economy can feel the repercussions. More initiatives banking 82 such as the Black Founder Accelerator Programmes by Barclays Rise will better harness the full potential of this significant entrepreneurial group. Support, mentoring and coaching are only part of the answer though, and FinTech could further benefit these founders by extending partnerships to accountants and other SME advisers. Collectively, these actions would help boost productivity, spur innovation, and generate economic uplift, further solidifying the UK's position as a global hub for business and innovation. 05| REDEFINING FINTECH SUPPORT AND FINANCING 90% of new start-ups go The dichotomy between FinTechs' growth focus and banks' caution presents a challenge to marry a successful partnership bankrupt and only 40% of between venturing and a historical desire for stable finances. FinTechs are young companies whose priority is not always to start-ups make a profit in become profitable, but to disrupt a market with an innovative technology or product. Startups can initially spend a lot of money on R&D, recruitment, and marketing (among other things) without generating any revenue. It often takes several years 81 for them to find a stable business model and become profitable, and this makes financing their ventures a challenge. With the their lifetime. 83 84 acquisition of the UK Silicon Valley Bank into HSBC’s Innovation Bank and the establishment of the FinTech Growth Fund to back the UK’s strongest growth-stage companies, there is a new dawn for FinTech and bank partnerships. This is something the UK will require if it is to respond to the call of the 2021 Kalifa Review of UK FinTechs for greater scale-up support and the estimated £1bn gap in growth stage funding. 43

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPeace FinTechs are a powerful contributor to a stable and accountable society 36% of FinTechs positively impact Peace in the UK by reducing illegal flows of money through KYC 85 (know your customer) and AML (anti-money-laundering) compliance technology. FinTech firms also lead the way in contributing to increased accountability and transparency of institutions through ESG, compliance and automated regulatory reporting, and protect fundamental information rights through innovative data protection solutions.

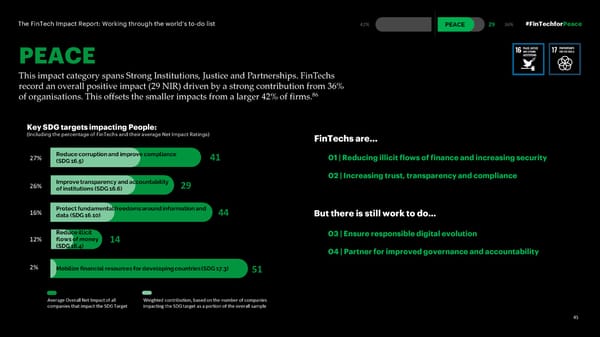

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPeace PEACE This impact category spans Strong Institutions, Justice and Partnerships. FinTechs record an overall positive impact (29 NIR) driven by a strong contribution from 36% of organisations. This offsets the smaller impacts from a larger 42% of firms.86 Key SDG targets impacting People: (Including the percentage of FinTechs and their average Net Impact Ratings) FinTechs are… 01 | Reducing illicit flows of finance and increasing security 02 | Increasing trust, transparency and compliance But there is still work to do… 03 | Ensure responsible digital evolution 04 | Partner for improved governance and accountability 45

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPeace 01 | REDUCING ILLICIT FLOWS OF 41% of FinTechs have a 26% of FinTechs significant impact on improving improve the transparency FINANCE AND INCREASING SECURITY the safety, accountability and and accountability of legitimacy of financial flows88 institutions89 The digital age comes with an increased need for data security and privacy, especially in the financial sector. FinTechs are at the forefront of technological innovation that helps organisations repel attacks and protect their AI digital identity verification (DIV) Onfido leverages AI, facial biometrics and customers’ data integrity. document verification to optimise DIV. Catering mainly to the financial and transportation sectors, it ensures compliance with KYC and AML rules. This assists in incorporating the nearly 40% of the global adult population who have At a time when the UK’s Corruption Perception Index (CPI) been excluded from banking due to insufficient identity proof. 87 is at its lowest ever level, FinTech can play a key role in harnessing advanced tools ranging from sophisticated NextGen compliance platforms: Compliance platforms and leveraging distributed financial crime detection to the likes of Onfido’s enhanced ledger technology has reduced the burden of due diligence. Umazi brings together biometrics for identity verification. data from multiple trusted industry sources into a complete company profile that can be used by businesses – without the need for multiple manual checks. The Companies such as Umazi have deployed innovative dynamic real time updates allow businesses to focus on growth rather than due diligence . integrations of blockchain and distributed ledger Data Exposure intelligence: Transforming the full corpus of exposed data into technology to drive greater transparency in due diligence. actionable insights, Lab 1’s AI, models and rating engine provides a comprehensive Others such as Lab1 are providing financial organisations real-time view of data risk for organisations and their supply chains. Helping with real-time monitoring of compromised data sets to them defend against attacks, fortify supply chains, protect customers from fraud and swiftly respond to hidden threats—ultimately minimising risks and costs. enable rapid response and intervention. Together these improve customer protection and reduce risk exposure. 46

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPeace 02 | INCREASING TRUST, 27% of FinTechs reduce corruption and TRANSPARENCY & COMPLIANCE improve compliance91 Trust is the bedrock of the perceived value of money and Catalysing industry trust through streamlined vendor selection: Eliminating the is critical to the financial sector. In an increasingly digitised traditional friction points between financial institutions and FinTech startups, world, fostering this trust requires transparency and TechPassport offers a unified, secure platform to expedite vendor partnerships and innovation. By co-developing a comprehensive, enterprise-ready questionnaire steadfast compliance. FinTech plays a key role in with 14 global banks, the platform not only simplifies the vendor selection process addressing these pillars, with 27% of FinTechs positively but also cultivates a culture of transparency, compliance, and trust across the impacting the SDG on corruption and improved financial sector. 90 Reducing corruption for trusted institutions: Behavox is a security software compliance. company specialising in communication surveillance. As a market leader in the application of Artificial Intelligence to monitor text and voice communications, Solutions range from the likes of Behavox monitoring Behavox’s software protects companies and their employees from illegal and behaviours and flagging non-compliance in capital malicious activities. markets trading, to due diligence on FinTechs themselves – something TechPassport has pioneered by using pre- onboarding checks to build confidence in FinTech firms among enterprise procurement teams. 47

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPeace But there is still work to do… 03 | ENSURE RESPONSIBLE DIGITAL EVOLUTION 35% of FinTechs are more at risk While the rise of FinTech brings immense promise, it is not without its challenges. It is imperative that the sector of providing illicit channels for engages with Regulators with the purpose of applying regulatory protection to new technologies and services, in a financial flows than large proportionate and agile way that supports innovation. It is encouraging to see evidence of this attention, such as the FCA issuing rules on the advertising of crypto-assets to ensure financial promotions are 94 institutions; they also have a fair, clear and not misleading . greater negative impact92 The goal of FinTech in this context is to ensure that the use of transformative technology serves as a consistent enabler of transparency and trust, and not a potential avenue for misuse. 04 | PARTNER FOR IMPROVED GOVERNANCE AND ACCOUNTABILITY The UK’s Financial Secrecy While 41% of the FinTechs we assessed were shown to have a significant positive impact on the safety, accountability and legitimacy of financial flows, it is also important to note that 35% were identified as being more at risk of providing Score is low; there is a need illicit channels for financial flows than large institutions and having a higher negative impact.95 This 35% is typically for more transparency and driven by early-stage digital payment platforms, including some digital currencies, which have shown vulnerabilities in 93 process and governance – in some cases, entire asset platforms have failed, in others they have been vehicles for accountability 96 ransomware payments with money laundering loopholes seeking to be exploited by criminals . Partnerships have the potential to balance innovation and governance. A FinTech solution can be paired with an established organisation’s well-regulated, process-driven controls to bring an optimum proposition to customers at scale, with creativity, security and compliance. 48

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPartnerships 05 |The Partnership Opportunity

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPartnerships Why duplicate effort across an industry when you can efficiently and rapidly partner on a set of underlying technology innovations? FinTechs have the potential to be the key bridge in helping traditional finance leverage its scale and reach to better meet the needs of a changing world through the adoption of the targeted, impactful solutions typically innovated by FinTechs. Encouragingly, financial institutions (FIs) are increasingly investing in multiple FinTech partnerships. This is driving a step-change in the impact FinTech can have. It is also opening-up a larger and more diverse set of customers to FinTech solutions, as well as proposition and productivity improvements for larger FIs. The Real Impact of FinTech Report

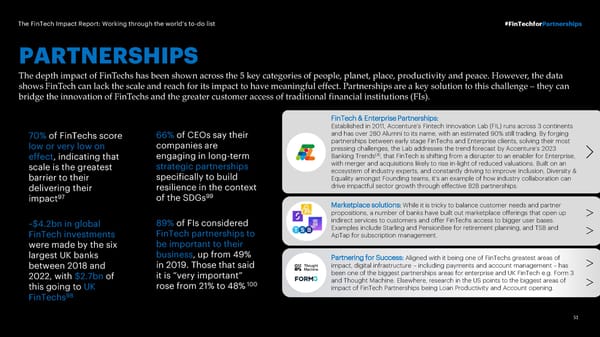

The FinTech Impact Report: Working through the world’s to-do list #FinTechforPartnerships PARTNERSHIPS The depth impact of FinTechs has been shown across the 5 key categories of people, planet, place, productivity and peace. However, the data shows FinTech can lack the scale and reach for its impact to have meaningful effect. Partnerships are a key solution to this challenge – they can bridge the innovation of FinTechs and the greater customer access of traditional financial institutions (FIs). FinTech & Enterprise Partnerships: Established in 2011, Accenture’s Fintech Innovation Lab (FIL) runs across 3 continents 70% of FinTechs score 66% of CEOs say their and has over 280 Alumni to its name, with an estimated 90% still trading. By forging low or very low on companies are partnerships between early stage FinTechs and Enterprise clients, solving their most pressing challenges, the Lab addresses the trend forecast by Accenture’s 2023 effect, indicating that engaging in long-term Banking Trends(4), that FinTech is shifting from a disrupter to an enabler for Enterprise, scale is the greatest strategic partnerships with merger and acquisitions likely to rise in-light of reduced valuations. Built on an specifically to build ecosystem of industry experts, and constantly driving to improve Inclusion, Diversity & barrier to their Equality amongst Founding teams, it’s an example of how industry collaboration can delivering their resilience in the context drive impactful sector growth through effective B2B partnerships. 97 of the SDGs99 impact Marketplace solutions: While it is tricky to balance customer needs and partner propositions, a number of banks have built out marketplace offerings that open up ~$4.2bn in global 89% of FIs considered indirect services to customers and offer FinTechs access to bigger user bases. FinTech investments FinTech partnerships to Examples include Starling and PensionBee for retirement planning, and TSB and ApTap for subscription management. were made by the six be important to their largest UK banks business, up from 49% Partnering for Success: Aligned with it being one of FinTechs greatest areas of between 2018 and in 2019. Those that said impact, digital infrastructure – including payments and account management – has been one of the biggest partnerships areas for enterprise and UK FinTech e.g. Form 3 2022, with $2.7bn of it is ”very important” and Thought Machine. Elsewhere, research in the US points to the biggest areas of this going to UK rose from 21% to 48% 100 impact of FinTech Partnerships being Loan Productivity and Account opening. FinTechs98 51

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact 06 |Concluding Call To Action

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact What drives the positive and negative impact? In short, we found a number of positive and negative traits that characterise the most impactful companies. Founders and CEOs can learn from these to help their organizations make a difference in the world. Impact Categories: Positive + Economic growth with scaled distribution + Sustainable financing for the things that matter + Regional offices to boost local economies (e.g. PEOPLE (e.g. available to a wider user base through Icon (e.g. the energy transition, affordable homes, and Icon access to new skill pools, job creation, taxes, Icon partnerships, rather than through self-build investment in SMEs) university collaborations, city cultures and uplifted which duplicates the industry effort) communities) + Simplified online presence end efficiency by + Inclusive services with low barriers to entry, served + Efficient infrastructure services (e.g. Icon design (i.e. low-energy-consumption websites at the point of need (i.e. minimal data requirements, embedded finance, banking-as-a-service rails and data processing) Icon convenient hours of service, low fees and PLANET Icon that boost productivity and enable wider consciously serving deprived regional areas and ecosystem capability and resilience) + Transparency of positive impact on the Planet fairly including minority groups) Icon (and across all dimensions e.g. climate, nature + Robust compliance and accountability (e.g. and society) + Financial education (i.e. open-access, non- to reduce illicit flows of finance through + Alternative lending models for wider, more presumptive, inclusively designed services PLACE digital ID, KYC and AML) Icon inclusive access to credit (e.g. based on Open particularly for underserved groups or available in Banking account transactions, rather than deprived regions) traditional agency credit scores) Negative × Lack of transparency (e.g. use of complex × Scaled data processing without lean algorithms × Limited governance and protection against fraud PRODUCTIVITY financial engineering, missing disclosures for Icon or purging of historically unused storage (e.g. avoiding gaps in governance and controls ESG decisions, a lack of cross-industry (particularly if not offset by the use of green caused by scaling too rapidly) collaboration and weak AML/fraud controls) energy and clean water programmes) × Funding industries that negatively impact × Innovations that drive up the cost of doing × Operating in unregulated domains (e.g. without SDGs (e.g. financing ‘business as usual’ Icon business or move affordability beyond the reach sufficient proactive industry engagement or PEACE natural resource exploitation and other tier 3 of the masses (e.g. property trading or customer protections to minimise financial stability heavy greenhouse gas emitters) inaccessible investment vehicles) risks posed by emerging innovations) × Losing focus on purpose and impact as scale takes over (e.g. business models focused primarily on Icon productivity, economic benefits and short-term shareholder returns rather than being balanced towards driving an increasingly positive impact on People, Planet, Place and Peace) 53

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact Financial services is a unique industry in its ability to support so many cross-cutting social issues for individuals; but also to be the industry that drives financing into the greatest “challenges the world faces. The growing requirements of regulators, and of society, to report not just how your “ company operates, but how it impacts the social and environmental issues around us, could position FinTech as the industry that can lead the way in terms of designing and building products and services that contribute to society and the world around us. Kimberley Abbott CEO & Founder, Vested Impact

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact Conclusions What we can do, together With 97% of UK FinTechs assessed contributing positively 2. Focus on our strengths harnessed successfully, FinTechs can be at the vanguard to the UN SDGs, the sector has been shown to be impactful There are also points to note on the impact of FinTech on of the UK’s growth in the next decade, uplifting people’s against the things that matter for our world. people and place. The contribution to inclusive offerings welfare and wellbeing. The sector’s overall impact against the SDGs is a and access to financial services has a meaningful impact. As FinTechs have a proven impact on the world, it is critical significantly positive one and, whilst its impact is less than However, FinTech has a limited ability to distribute to a that they are nurtured independently and through key sectors such as education for example, it outperforms wide customer base and operate at scale. Traditional partnerships, with the right investments, fairer others such as retail, capital markets and construction. financial institutions may have less of a propositional representation of founders from diverse backgrounds and Based on our research, Productivity is the most impacted impact, but this is spread across a wider range of places an uplift in women in the workforce beyond the current area of SDGs, with 98% of the assessed FinTechs making a and a greater number of people. 28%. Together, this will accelerate the sector’s growth and positive contribution. The positive impacts of FinTech 3. Partner and invest drive positive changes to society and the planet. extends beyond economics though, with notable benefits For these reasons, the prospect of more partnerships with 4. Take action to harness our productive potential also identified against the things that matter most for enterprise firms offers a route to even greater impact in the The prospect of FinTech having an even greater impact people, place and peace – such as reducing transaction future. By combining the innovative and impactful than it currently does is undeniable. costs, enabling new infrastructure and developing security solutions of FinTechs that operate at the cutting edge of controls. financial services with the scaled reach and robust Now is the time to ask… 1. Save the planet governance of larger institutions, the true impact of WHAT CAN YOU DO TO CHAMPION THE CONTINUED We have shown that despite a very strong positive impact FinTech could be unlocked and the risks to financial SUCCESS OF FINTECHS ACROSS THE UK? on the planet from 9% of UK FinTechs, the sector overall stability and customers from emerging technology #ForCustomers #ForFounders #ForThePlanet has a negative impact. This cannot be ignored, particularly mitigated. This would benefit the UK in many ways. when you consider that financed emissions associated with There is encouraging movement toward this collaboration investing, lending and underwriting are on average over for scale – we have seen the FinTech Pledge, the Kalifa 700 times higher1 than an organisation’s direct emissions. Review of UK FinTech, The FinTech Growth Fund and now Capital markets and finance must align to environmental the Centre for Financial Innovation and Technology (CFIT) goals, deploying capital towards a transition to being formed and mobilising to address specific financial sustainability and positive impact, and thereby de-risking industry challenges for customers. investments. By combining impact data and finance flows FinTechs have the power to sustainably boost our to enable tangible change, FinTech has a huge role to play productivity in the UK, at a time when the national and must rise to this challenge. economy is battling to achieve productivity targets. If 55

The FinTech Impact Report: Working through the world’s to-do list #FinTechforImpact Get in touch with us Graham Cressey | Director, FinTech Innovation Lab Sacha Brereton | Programme Lead, FinTech Innovation Lab graham.cressey@accenture.com | sacha.brereton@accenture.com Accenture is a leading global professional services company that helps the world’s top businesses, governments and other organisations build their digital core, optimise their operations, accelerate revenue growth and enhance consumer services – creating tangible value at speed and scale. Janine Hirt | CEO Adam Jackson | Policy Director Roberto Napolitano | Director of Marketing & Communications janine@innovatefinance.com | adam@innovatefinance.com | roberto@innovatefinance.com Innovate Finance is the independent industry body that represents and advances the global FinTech community in the UK. Its mission is to accelerate the UK’s leading role in the financial services sector by directly supporting the next generation of technology-led innovators. Kimberley Abbott | CEO and Founder kim@vestedimpact.co.uk Vested Impact is an award-winning data company that has redefined “millionaire” to be a person who impacts millions of lives. It quantifies the outward impact of companies on the world’s greatest challenges; leverages 300 million science-based data points to automatically assess and quantify the impact of companies and investments; and empowers companies and institutions with the data to manage impact risks and opportunities. Alex Craven | CEO Fatima Garcia | Chief Data Scientist alex.craven@thedatacity.com | fatima.garcia@thedatacity.com The Data City is a tech company that maps sector, cluster and company growth in the UK using an AI-driven platform of over 5 million businesses and 350 emerging economy sector classifications. Their industrial classification system allows policymakers, economists, investors and analysts to understand the emerging economy and markets in real time.

***Confidential*** Appendices